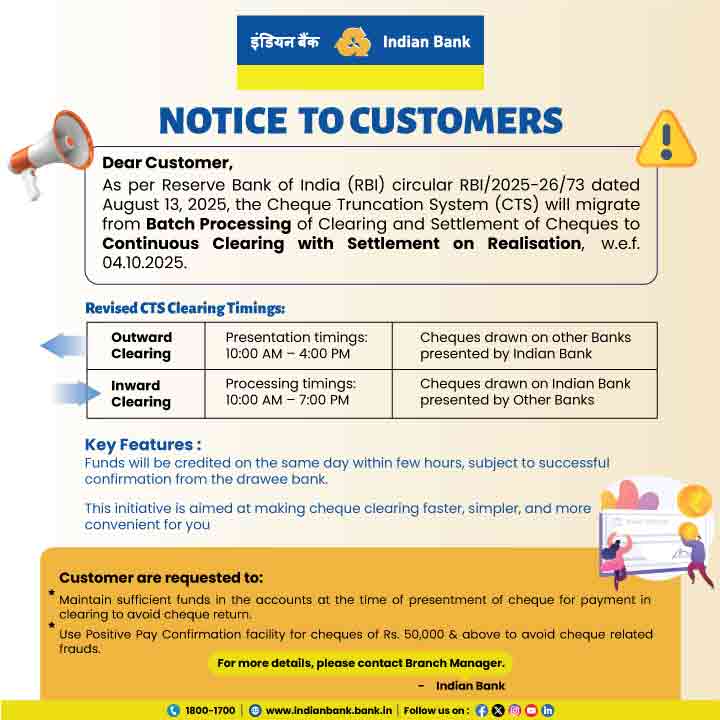

What is Form 121? A Simple Guide to Avoiding Unnecessary TDS

Tax Deducted at Source, commonly known as TDS, is a mechanism through which tax is collected at the point of income generation. Banks deduct TDS on interest earned from fixed deposits and certain other deposits when the interest exceeds the prescribed threshold limit. However, not every depositor is required to pay tax on such income. For eligible customers, submitting Form 121 (earlier known as Form 15G / Form 15H) can help avoid unnecessary TDS deduction.

This blog explains the purpose of the form, who can submit them, and how they help customers manage their finances more efficiently.

What is TDS on Bank Deposits?

When the total interest earned on fixed deposits, recurring deposits or similar schemes crosses the limit specified under income tax rules in a Tax year, banks are required to deduct TDS before crediting the interest. This deduction is made even if the depositor’s total income is below the taxable limit.

In such cases, the depositor may later claim a refund while filing an income tax return. However, this process can affect immediate cash flow. To prevent such deductions in the first place, eligible individuals can submit a self-declaration using Form 121.

What is Form 121?

Form 121 is a new, unified self-declaration form effective April 1, 2026 that replaces old Forms 15G and 15H to prevent TDS on specific incomes. It allows eligible taxpayers to receive specified incomes such as interest on deposits, dividends, or rent, without TDS, provided their estimated total income for the tax year is below the taxable limit. These declarations are made under Section 393(6) of the Income-tax Act, 2025 read with Rule 211 of the Income-tax Rules, 2026.

Form 121 also simplifies the declaration process by replacing both Form 15G and Form 15H with a single form. This means taxpayers no longer need to determine which form applies to them based on age, as Form 121 can be used by all eligible resident taxpayers.

Form 121 can be submitted by:

- Resident Individuals (below 60 years)

- Resident Individuals (60 years and above)

- Resident HUFs

- Specific Eligible entities

Form 121 cannot be submitted by:

- Companies

- Firms

- Non-residents

Form 121 can be submitted if:

- No tax liability for the year

- Total interest income below the basic exemption limit

- Estimated total income below the taxable limit after considering deductions (Resident individuals aged 60 years or more)

Income Types Covered

Form 121 can be used to prevent TDS on the following types of income, subject to eligibility conditions:

- Interest from bank fixed deposits (FDs) and recurring deposits (RDs)

- Interest from post office schemes

- Dividends from shares and mutual funds

- Insurance commission and rental income

By submitting Form 121 at the beginning of the Tax year, eligible customers can ensure that TDS is not deducted on their deposit interest. The form must be submitted before the income is paid or credited, as late submissions will not prevent TDS already deducted.

When Should Form 121 to Be Submitted?

Ideally, Form 121 should be submitted at the start of each Tax year. If a new deposit is opened during the year, the form should be submitted at that time to avoid TDS deduction.

It is important to note that this form must be submitted on every tax year. A declaration given in one year does not automatically apply to the next year.

Upon successful submission of Form 121, an acknowledgement is shared with the account holder.

Important Points to Remember

- Customers must provide accurate details such as PAN, estimated income and deposit information while submitting the Form 121. Providing incorrect information or making a false declaration may attract penalties under income tax provisions.

- Quoting of PAN is a mandatory requirement for submission of declaration in Part A of Form No. 121 by the declarant. In the absence of PAN, the declaration is invalid and the payor is required to deduct TDS at the applicable rate as per Income-tax Act, 2025.

- Form 121 can usually be submitted at the branch or through digital banking channels, subject to bank procedures.

- Form 121 is simple yet effective tool that help eligible customers to avoid unnecessary TDS on interest income. By understanding the eligibility criteria and submitting the correct form on time, customers can improve cash flow and reduce the need to claim refunds later.

- Before submitting Form 121, it is advisable to assess total income (Old Tax regime / New Tax regime as the case may be) and estimated tax liability for the Tax year. Responsible declaration ensures compliance while enabling better financial planning.

- If you have FDs in multiple banks, Form 121 must be submitted to each bank individually.

- Submitting Form 121 does not make income tax-free; it only prevents TDS if the eligibility conditions are met.

Indian Bank. “Your Own Bank, Always with You”

Disclaimer: https://indianBank.Bank.in/departments/disclaimer/

{kind=link}